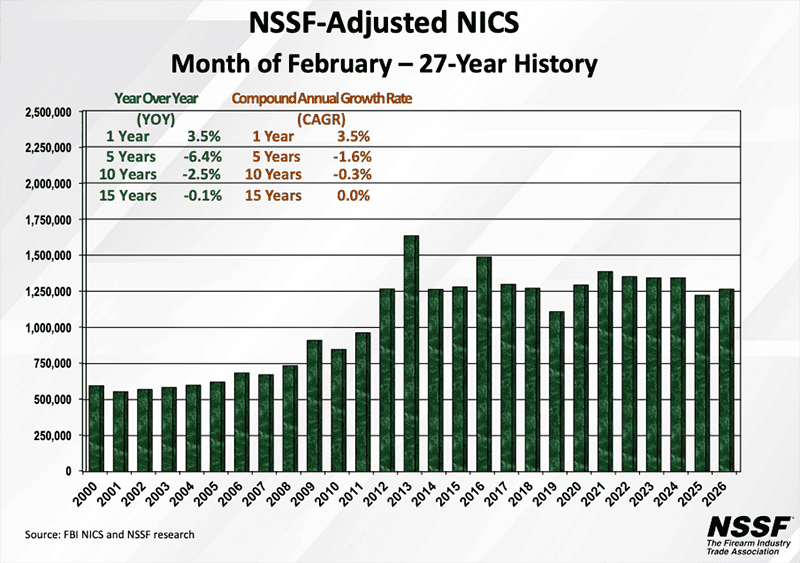

February’s NSSF-adjusted NICS figure clocked in at 1,265,320—a solid 3.5% bump from last year’s 1,222,000-ish mark—signaling that Americans aren’t hitting the brakes on their Second Amendment enthusiasm. This isn’t just a raw number; it’s the gold standard for tracking firearm background checks after the National Shooting Sports Foundation strips out non-purchase noise like concealed carry renewals and peep hunts. Coming off a holiday-season slowdown, this uptick screams steady demand amid a cocktail of economic headwinds, urban crime spikes, and the ever-present drumbeat of federal overreach threats. Think about it: with inflation still biting and red-flag laws creeping into more states, folks are voting with their wallets (and trigger fingers) for self-reliance over reliance on 911 response times that feel like eternity.

Digging deeper, this modest growth masks some fireworks. Historical context? February NICS often plays catch-up to January’s post-New Year’s rush, but a 3.5% gain here outpaces the sleepy 1.2% yawn from February 2023. It’s no 2020 frenzy (when checks exploded 40%+ amid riots and lockdowns), but in a post-pandemic market flooded with supply, it hints at organic, non-panic buying—likely long guns for home defense and hunting season prep, plus a surge in first-time buyers spooked by border chaos and schoolyard headlines. For the 2A community, the implication is crystal: manufacturers like Ruger and Smith & Wesson can breathe easier with sustained retail velocity, FFLs are stacking inventory wins, and grassroots orgs like GOA and NRA have fresh ammo to lobby against Biden-Harris sequel schemes. Steady is the new surge.

Bottom line? This data drop is a quiet middle finger to the gun-grabbers peddling assault weapon myths—proving the right to keep and bear arms isn’t fading, it’s fortifying. If March builds on this, expect Q1 to hand the industry its strongest opener since the China virus scramble. 2A warriors, keep stacking those brass; the momentum’s yours.